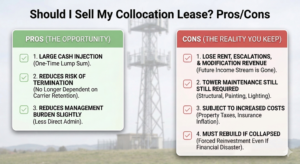

If you own towers with DISH as a tenant, you’ve probably already felt the pain—or you’re about to. Here’s what we’re seeing in the market and what it means for you.

What Buyers Are Paying (Or Rather, Not Paying) for DISH

Let’s start with valuation, because this is where it hits hardest. While buyers were already discounting DISH revenue somewhat, they are no longer attributing any value to it. Zero. And the reason is simple—

most tower owners aren’t being paid on their DISH leases right now, and few expect to receive anything in the future. The revenue has effectively already disappeared for many owners, so the tower’s cash flow (TCF) is accordingly lower.

The market expects DISH equipment to be abandoned in place, meaning tower owners will eventually be on the hook for removal costs. That’s a cost, not a benefit. The silver lining—and there is one—is that when that equipment does come down, it frees up a RAD center on the tower. For a well-located tower, that’s a real opportunity. But a buyer will assume some sort of cost to remove the equipment in the future. (or plan on requiring an inbound tenant to remove it.)

The Lease-Up Story Gets More Complicated

Here’s something that doesn’t get talked about enough: DISH was responsible for somewhere between 30% and 50% of new colocation lease activity between 2021 and 2024. That’s a massive share of the new revenue that was driving lease up expectatins and tower valuations higher. With DISH (and US Cellular) effectively out of the market, that pipeline of new leases doesn’t just slow down; it takes a hit. (

See CCI’s last earnings report and subsequent stock decline, and AMT’s recent earnings, where it indicated that DISH represented 20% of new leasing activity.)

Going forward, tower lease-up should be more muted. Not dead, but don’t expect the same pace of new amendments and new leases we saw during peak DISH buildout activity.

What About AT&T and DISH Network?

The AT&T acquisition of DISH spectrum (700 MHz and C-Band) is still underway, but assuming it closes, the natural question is whether AT&T’s deployment of those acquired DISH frequencies will generate new revenue for tower owners. Our honest assessment—we’re skeptical it will move the needle much.

AT&T’s acquisition of additional spectrum may actually reduce its need to densify its macro network in high-capacity areas. More spectrum can mean greater efficiency on existing infrastructure, leading to fewer new macro sites needed. That’s not the growth story tower owners are hoping for.

There could be some incremental amendment activity as AT&T integrates new equipment to handle those frequencies, but we wouldn’t underwrite significant new tower cash flow as a result.

The Bottom Line

Of late, DISH has been a headwind for tower valuations, driven by lost current revenue, future removal costs, and a slower lease-up outlook. If you own towers with DISH tenants, it’s important to enter any sale process with realistic expectations about how buyers are underwriting that revenue (or not). The good news is that well-located towers with strong anchor tenants still have solid fundamentals. The bad news is that TCF on towers with DISH will decline, and overall lease-up (especially on number of new collocation leases) will decline.